SECURE YOUR CROSS-BORDER TRADES WITH OUR SBLC, BG AND BLOCK FUNDS SOLUTIONS BY SWIFT MT799 AND SWIFT MT760 DELIVERY

April 1, 2025 7:39 am

SECURE YOUR CROSS-BORDER TRADES WITH OUR SBLC AND BG SOLUTIONS BY SWIFT MT799 AND SWIFT MT760 DELIVERY

Bank Collateral Provider and Private Banking.

We do not SALE or LEASE the Bank instruments. If a Bank instrument is leased, it will not be permitted for use in loans, credit, or hypothecation. Furthermore, leasing of Bank instruments or assets in bank accounts is strictly prohibited. Instead, we request our Bank to issue the SBLC, reserved and assigned in favor of the client’s nominee beneficiary.

What is a Standby Letter of Credit (SBLC) and Bank Guarantee BG is a legal document that provides assurance to a seller that they will receive payment from a bank in case the buyer fails to fulfill their obligation under a trade agreement. It is especially useful for international trade where parties may not be familiar with each other’s laws and regulations. By issuing an SBLC, the bank acts as a neutral third party, helping to facilitate secure transactions and mitigate risks for all parties involved.

Standby letters of credit SBLC and Bank Guarantee BG are common tools used in international cross-border trade, but the requirement for collateral can impede cash flow, which may restrict the pursuit of new ventures or starting work. However, utilizing standby letters of credit collateral can provide a viable solution to obtain funds effectively.

At our company, we do not lease or rent out Bank Instruments. Instead, we assign it to our nominated clients, granting them full privileges of use for their loan, credit line, trades, project funding and etc… We may also consider joint ventures with clients, in some cases to share the risk, subject to specific conditions. Each case is evaluated on its own merits, and our board will make informed decisions accordingly.

Bank loans are usually the least expensive way to finance a business, trades, project funding, etc. However, it is not easy to get a bank loan, as banks have strict standards for lending. As a general rule of thumb, banks will require a borrower to put up collateral for a loan. The only exception to this rule is for clients who have a long-term relationship with banks and whose business has proven to be profitable over a multi-year period.

Collateral is important for banks to reduce their risk. If the business is not able to pay back the loan, a bank may decide to take ownership of the collateral that has been pledged to them in the documents you sign when you got the loan.

Usually, a bank will not take ownership of collateral if you miss an interest payment or one or two repayment installments, but will if they feel that their loan is at risk. Collateral plays a crucial role for banks in mitigating risk. It serves as security for the loan, allowing the bank to take ownership of the pledged collateral in case the borrower defaults on the loan. Typically, banks won’t immediately seize collateral after a missed interest payment or a couple of missed installments, but they may take possession of it if they believe their loan is in jeopardy.

In general, banks prefer to have collateral that is easily converted into cash, such as deposits, cars, equipment, or real estate. Their advance rates against these assets will be higher than against inventory or receivables, which are much harder to convert into cash.

THE EFFECTIVE UTILIZATION OF SBLC COLLATERAL THROUGH MT799 AND MT760 DELIVERY

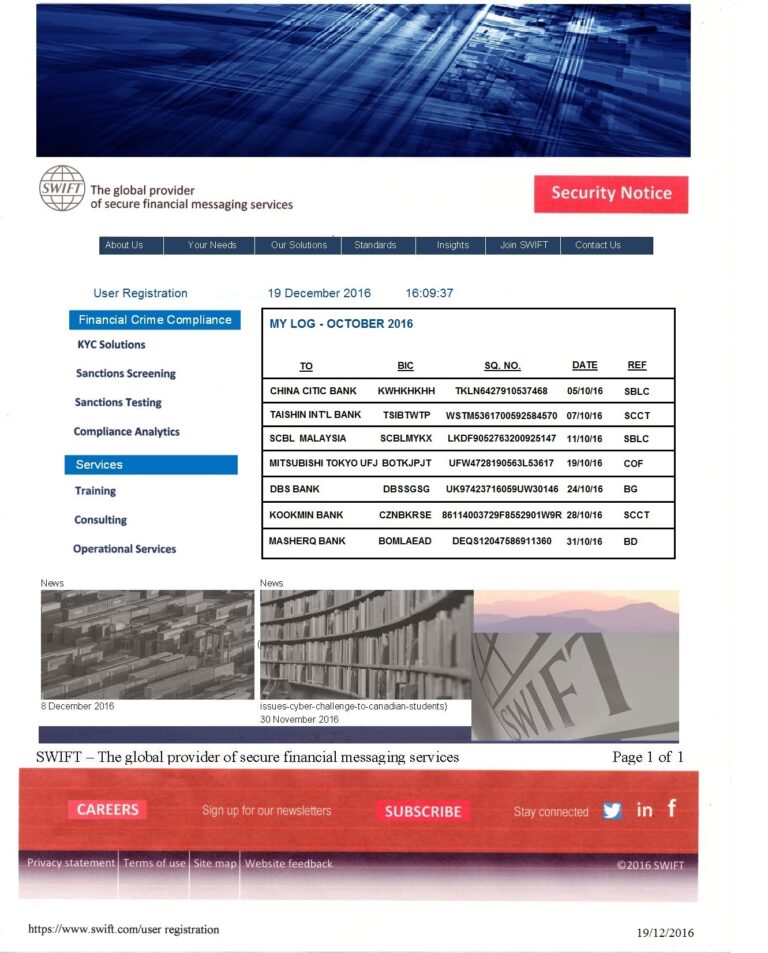

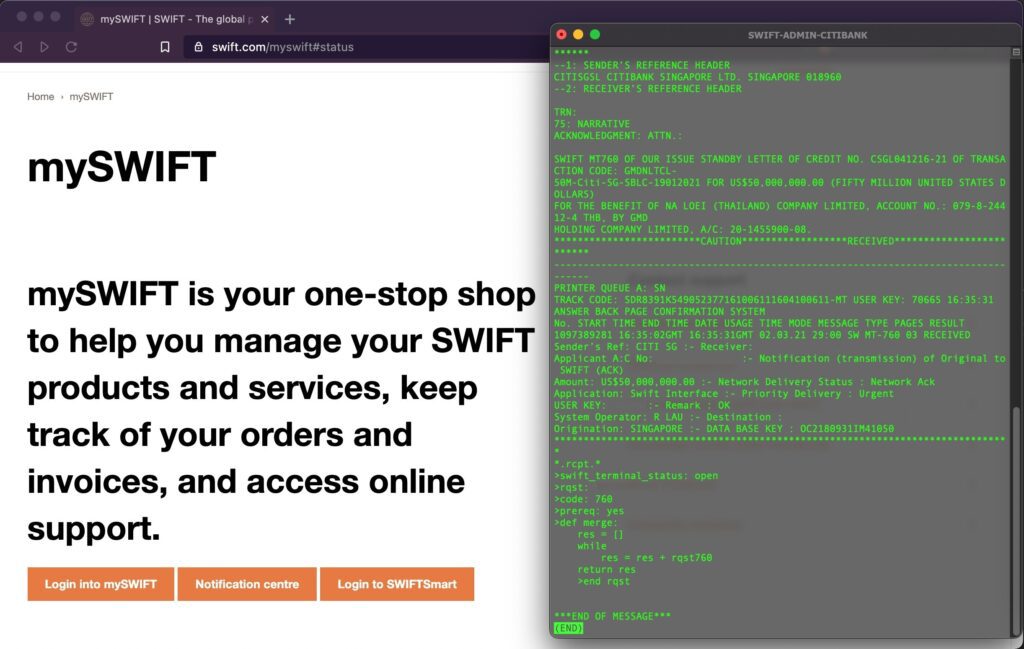

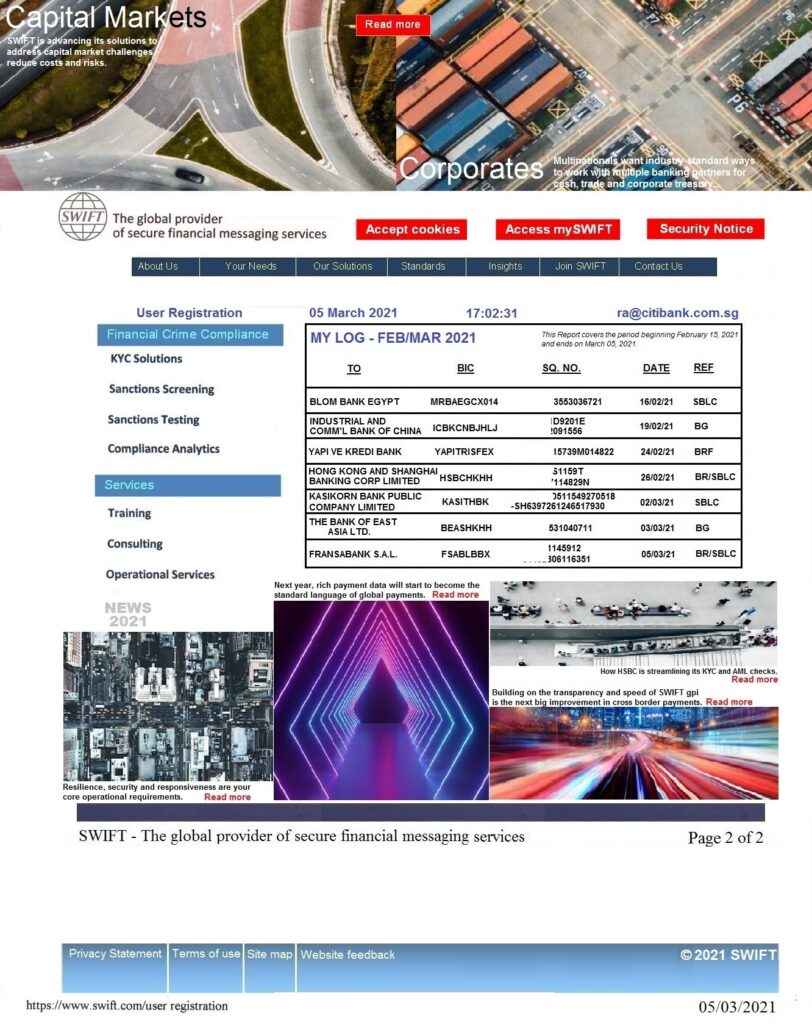

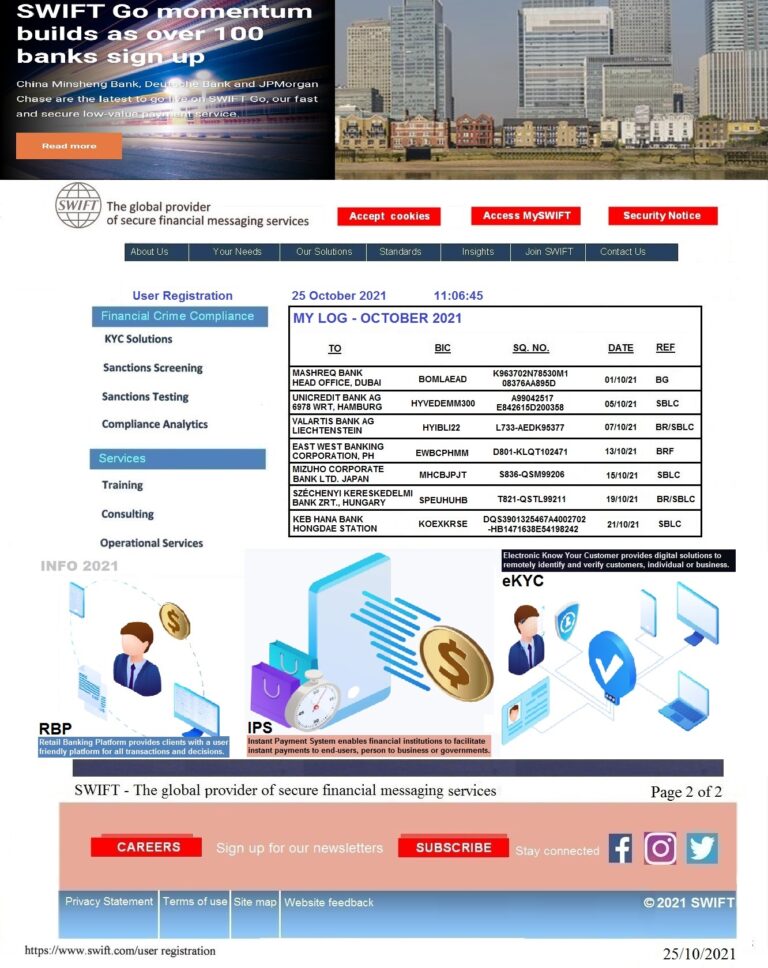

Our Private Banking service with a track record offers a robust financial solution utilizing fully cash-backed SBLC collateral or Bank Guarantee BG from the top 20 banks in the world. The collateral ranges from a minimum of 50 million to 500 million USD and has a term of one (1) year, which can be extended up to three (3) years. Denominations are available in USD or Euro, and delivery is pre-advised by MT799 and MT760. Our collateral is versatile and can be used in a variety of areas, including petroleum, gas, aviation fuels trading, real estate development projects, and commodities such as sugar, cereals, cocoa, coffee, gold bars, precious stones, and large volumes of consumer goods. It’s important to note that swift cost, underwriting cost, and bank fees must be PREPAID before the delivery of Swift MT799 and MT760.

Proof of Fund (POF) Via Swift MT 799 and Bank to Bank Bonded courier.

MT 760 SBLC and BG

MT 760 Blocked Funds Instrument

If the client request for face to face meeting, there is an engagement fee required, which is prepaid the invoice for meeting regarding the Banking matters.

To pre-qualify, clients are required to provide a client information sheet, corporate documents indicating good standing, and bank details for the receiving party, as well as demonstrate the capacity to cover the PREPAID issuing cost.